Fundamentals to support Rand?

In last week’s Part 1 of this column we showed that there has been a very close correlation between the Rand/US Dollar exchange rate, the oil price and the JSE Allshare index. As the oil price (and commodities in general) rose, the Allshare index rose while the Rand weakened. Now that the oil price (and commodities in general) collapsed, the Allshare index appears to be stagnating where its close correlation with the oil price would have indicated at least a significant decline in the Allshare index.

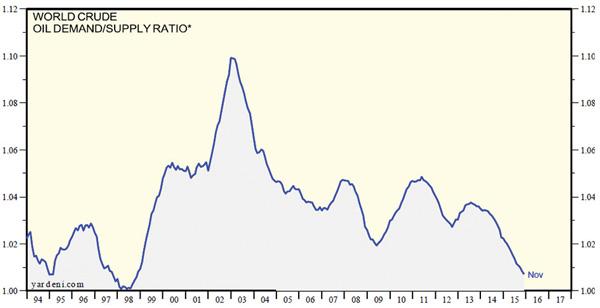

12 month average world oil demand

It would have similarly indicated a strengthening of the Rand whereas the Rand has actually weakened significantly. History does indicate though that the Allshare index appears to ignore rapid changes in the oil price and the Rand/US Dollar exchange rate and that the recent swings in their fortunes may not necessarily lead to the index retreating significantly.

As we conclude above, the recent collapse in the oil price does not appear to be justified, which may be the reason for the Allshare index not having tracked this collapse. Similarly it appears that the recent ‘collapse’ in the Rand/US Dollar exchange rate is not justified.

On this basis, we conclude that the weakness of the Rand is overdone and that the Rand should strengthen on the basis of fundamentals. However this weakness is bound to result in an increase in the SA repo rate sooner and higher than expected. We also believe that it is bound to accelerate the rate of inflation which also will lead to an increase in the repo rate. , Finally, we believe that the weakness of the oil price (and commodities in general) is overdone and should reverse. However this reversal may take quite a while to manifest.

While we are faced with these very negative developments for which it is very difficult to time a correction, the investor should continue to focus on real returns rather than absolute returns to increase his wealth slowly and steadily. With an inflation rate of around 3% one should be quite content if one manages to achieve an investment return around of 8% per annum. As an active fund member one should not shun equities but should be cautious, spread the risks as far as the law allows and focus on stock picking. In terms of equity sectors, depressed commodity markets may offer selective buying opportunities but this may require patience to realise gains, and it may still just be too early. Consumer Goods and Consumer Services had a terrific run since the beginning of 2006, driven mainly by foreign investors. With the severe depreciation of the Rand, foreign investors will have been hurt and their interest is likely to wane. We therefore do not see much potential in these sectors any more. This leaves the Financial and Industrial sectors as sectors we believe to offer the best prospects.

In terms of diversification between different asset classes locally, the likelihood of a repo rate increase suggests that interest bearing investments do not hold good prospects at this stage. However the prospect of accelerating inflation favours inflation linked bonds.

Although global diversification must be part of any local investor’s investment strategy, the overdone weakness of the Rand suggests that one should currently not move capital offshore. More speculative investors with offshore investments may actually want to consider repatriating capital to capitalise on what we believe to be an unjustifiably weak Rand.

{kind=link}