National reinsurer, one of only a very few state-owned enterprises ripe for listing on the Namibian Stock Exchange

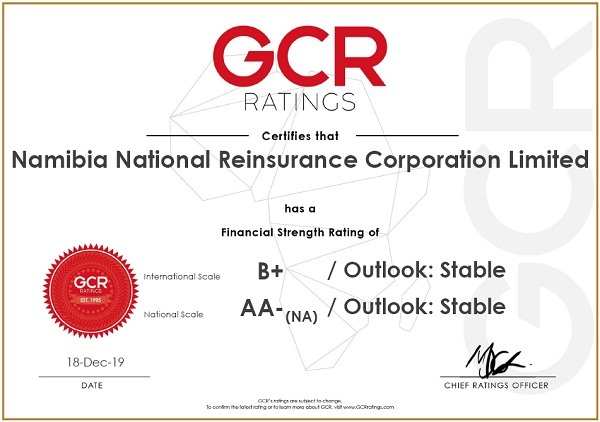

The African division of Global Credit Ratings Co. (GCR) released the updated credit rating for the national reinsurer, Namibia National Reinsurance Corporation Ltd (NamibRe), this week, confirming its national financial scale strength rating as investment grade but moving it one notch higher from A+ to AA- with a stable outlook.

On the international scale, NamibRe’s rating also improved from BB to B+, also with a stable outlook.

Global Credit Rating Co. was founded in 1996 as the African arm of the New York Stock Exchange-listed Duff & Phelps. Very rapid growth followed and within only a short period the group established itself as the market leader, accounting for the majority of all ratings accorded on the African continent. GCR’s African regional headquarters are based in Johannesburg, with its main SADC, West, and East African regional offices in Harare, Lagos and Nairobi respectively.

In its NamibRe review, GCR stated that it had released new criteria for rating insurance companies in May 2019. Consequently, the ratings for NamibRe were placed ‘Under Criteria Observation’. GCR finalised the review for NamibRe under the released Criteria for Rating Insurance Companies, May 2019. As a result, the ratings for NamibRe have been reviewed in line with the new methodology and subsequently removed from ‘Under Criteria Observation’.

“NamibRe’s national scale financial strength rating upgrade reflects sustained improvement in earnings, together with maintenance of strong risk adjusted capitalisation and liquidity. These credit strengths are partially diluted by a relatively limited business profile.”

“The improvement in earnings was supported by a favourable claims experience, together with sound investment income. As such, the three-year aggregated underwriting margin equated to a higher 13% (FY19: 18%; FY18: 17%), compared to the prior three year cycle margin of 4% (FY16: 5%; FY15: 3%).”

“Furthermore, the return on revenue equated to 19% in FY19 (FY18: 19%: FY17: 9%).”

“Going forward, GCR views the maintenance of a favourable claims pattern, coupled with consistent investment returns as key drivers for earnings to be sustained within a strong range. Risk adjusted capitalisation is viewed to be strong, with a large capital base catering for the quantum of insurance and market risk exposures. Risk adjusted capitalisation may remain at similar levels, albeit note is taken for potential moderation, should mandatory cessions resume on the back of the legal dispute being settled in favour of NamibRe. Liquidity is viewed to be strong, underpinned by healthy internal cash flow generation and conservative investment allocation.”

“However, the coverage of net technical liabilities by cash and stressed financial assets equated to a lower 2.9x at FY19 (FY18: 4.6x) due to reserving adjustments, while operational cash coverage registered at an unchanged 14 months.”

“The Stable Outlook reflects expectations of persistent financial profile strength while maintaining a comparatively limited view on business profile.”

“Upward rating movement is unlikely to develop over the medium term. Conversely, negative rating pressure may stem from reduction in risk adjusted capitalisation and liquidity beyond expectations. Furthermore, earnings pressure may result in negative rating movement,” stated GCR.

{kind=link}