Volatility is back. What impact is reasonable to expect in local markets?

Severe volatility in international markets mirrored by an ever-declining Allshare index of the Johannesburg Securities Exchange, raised the question among analysts whether we are set for a repeat of 2008 to 2010 when all markets worldwide gyrated wildly.

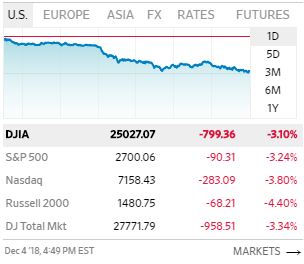

Last week, on 04 December, US markets went into a tailspin, plummeting between 3% and 4% in a single day. The downward trend continued on and off for another three days with investors holding their breaths just how far this correction will go.

This week Monday we celebrated Human Rights Day in Namibia, taking me out of my daily market watch, but big was my surprise on both Tuesday and Wednesday, when non-US markets staged somewhat of a comeback.

However, when I checked the actual index values on Wednesday, the surprise was even bigger when I noticed that the Dow has dropped another 560 points since last week’s calamitous Tuesday when the drop was a whisker shy of 800 points. The same trend was reflected in all the other major indices. The S&P is down by another 70 points, the Nasdaq by about 150 points, the Russel 2000 by 40 points with the Dow Total Market at an uncomfortable 27101, down by 600 points in five trading days.

I was expecting some regained ground from all these indices, yet the opposite transpired. To demonstrate just how severe the volatility continues to be, one only needs to look at the markets in Asia and at the FTSE. The Nikkei is back approximately where it was 9 months ago while both the Hang Seng and the Shanghai are substantially below their highs of 11 months ago, Even the FTSE, jumping more than one percent on Wednesday, was still stuck below 7000 index points, and very far from the lofty 7600’s earlier this year.

In our local markets, the two biggest events with a significant impact was the South African Reserve Bank’s decision to increase its repo rate from 6.5% to 6.75%, bringing it on par with the Namibian rate. Of course, the Bank of Namibia did not budge, opting to keep the rate at 6.75%, hoping that the SA move would be sufficient to support the currency.

Whether that was successful or not, is subject to opinion. There was a brief improvement in the Rand’s external value but this week it was back to the mid-R14’s with the JSE Allshare hovering above 51000 but very far away from the 62000 level in January this year.

During this year, there was much talk about a market correction but little reference to volatility. Although I chewed through one or two reports that warned of volatility, none saw it as a major threat. Instead, the question that I encounter most often revolves around the issue of a major market correction, say 20% or more.

There are several US analysts who expects a major correction, and there is the odd voice warning of another financial meltdown, but I sense these sentiments are based more on technical analysis and not on trading values. This boils down to a view that expects the market to correct, simply because it has expanded for ten years in a row. Sort of like a statistical probability – if it has grown so much for so long, history predicts that it has to contract again.

Fortunately, there are also sober analysts who stress that this is impossible to predict and that the only sensible strategy is to hold positions only in relation to their risk. Obviously, this brings me back to volatility for the more volatile the trading environment, the higher the risk.

Going by only one week’s trading history one certainly can not say that a correction has started. There is as yet, no factual basis for this. There is however, a very clear escalation in volatility and this may or may not portend a correction.

Equally speculative are the many opinions on what a correction will look like. Also for us, what the local impact of a worldwide correction will be?

It is dangerous to make dogmatic predictions but I think it is safe to expect that a major financial correction in the rest of the world, will have a definitive impact on the JSE directly, on the exchange rate indirectly, and on the Namibian capital market in a round-about way when investors shun Namibian instruments looking for better yield in other markets.

This much was already alluded to in the Bank of Namibia’s statement last week that accompanied the repo announcement. The bank made a point of local liquidity in the banking system, showing that it has deteriorated compared to the first nine months, but then again, by Wednesday it was back above N$3 bn and BoN Bills have dwindled to a mere N$50 million.

Do these pointers qualify as signs of local volatility? I doubt it. Our own banking system is stable, in a far better condition than the first half of 2017, and actually nibbling again on new credit. Will foreign market volatility have an impact on the JSE? Undoubtedly yes, but then do not forget that the Rand often appreciates when the rest of the market suffers.

Index values courtesy of the Wall Street Journal – Ed.

{kind=link}