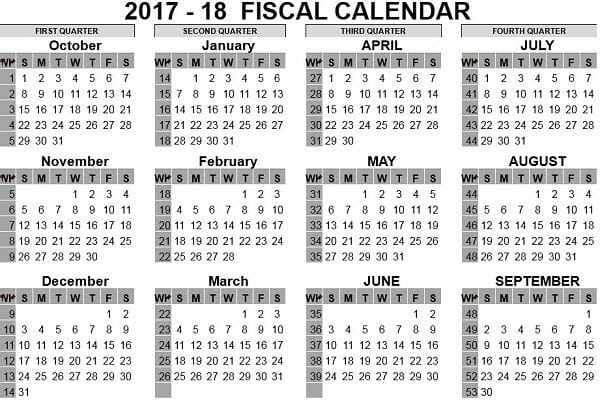

Skip March and move the beginning of the fiscal year to July

A good case can be made out for changing the cycle of the fiscal year. Not only will this reduce the pressure on the Ministry of Finance, it should also provide a more realistic picture of how the ingrained local business cycle impacts government finances.

As a matter of fact, one can argue that the Minister of Finance has already de facto changed the fiscal cycle in the way that he handled the budget for the past two years.

In March 2016, although the fiscal consolidation decision has already been taken officially, we received a budget that was still very much aligned with its lofty 2010 to 2015 predecessors where fiscal income nominally grew by around 18%. It was only during the course of the year, specifically during the second semester, that the budget constraints started surfacing, and the need for belt-tightening, as the minister called it, arose.

This lead to a momentous mid-year budget review on 27 October last year where the main budget was basically wiped off the table, replaced by a completely reworked 2016 budget and a drastically adjusted medium term expenditure framework.

Come the first week of March this year, that mid-year review budget, with minor cosmetic trimmings but zero substantial adjustments, were presented as the main budget for 2017. The frontloading done at the end of 2016 set the new levels for expenditure, and the new revenue estimates, closely followed in the 2017 budget.

However, the same change of tack revealed itself in the recent mid-year review, only now the direction was reversed. The expenditure targets underwent some rather significant adjustments and the medium term expenditure framework was again completely reworked to support the temporary suspension of the fiscal consolidation process.

In reality, the minister gave us the main budget for this year, already last year October and I suspect the same thing is going to happen in March next year. That should be a clear indication that the budget cycle is out of sync with the real economy.

If the fiscal year runs from July to June, it aligns itself with the financial years of many of the very large companies, including the banks. That should by itself be a fairly compelling argument to synchronise the fiscus with the private sector. Furthermore, the dead January February period immediately before the new budget is due, will then be much less of a headache. I believe that is exactly the reason why so many big companies chose a July June financial year.

If the fiscal year also runs July June, then the ministry can take two months to table the new budget somewhere near the middle of September. Then there is no rush and it really would not matter if the budget is advanced or delayed by a week or two. This then provides a far more reliable footing for the dreaded annual so-called Article IV consultation with the International Monetary Fund. Much of these discussions are based on future expectations which, I believe, will leave more room for adjustments, if necessary, in the mid-year review which will then fall somewhere near the end of March.

In short, shifting the fiscal cycle will relieve the early-in-the-year pressure, it will neutralise the end/beginning of the year slump, and it will give us longer lead times to prepare for the inevitable meetings with rating agencies.

I further believe that, given the fundamental rigidity of the budgetting process, it will provide the ministries with a flexibility they do not have under the current dispensation. Their individual expenditure cycles will then easier absorb the end/beginning of the year disruption, and they will be able to plan their spending more accurately, as they will now have to cover only three to four months in the second calendar semester, and a more contiguous eight-month term in the next calendar year.

Sovereign budgets do not come to a standstill at the end of a fiscal year, except when you have run out of money like in March this year. Budgets are by methodology designed to foster a certain, reliable, trustable continuity. They never actually stop, they carry on, from year to year all the time, and when the opportunity is there to take a snapshot, almost like an audit, it is so long after the events, it becomes mostly irrelevant, other than for academic purposes.

In essence, I believe the minister has already done this. His actions at least show that this is what happened in 2016 and 2017. Now it is only a matter of getting his colleagues to consent to change the law so that he can table the main appropriation bill at a more reasonable and practical time of the year.

PS: First, as an aside, is the City of Windhoek going to change Robert Mugabe Avenue back to Leutwein Street. I hear such rumours, or maybe they are just wishful thinking. Second, when will SADC start the consultative process to re-instate the SADC Tribunal?

{kind=link}