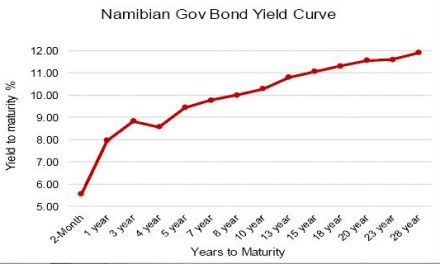

When it no longer helps to google the trade statistics

The gravy train is coasting along without gravy. Last week the IMF team leader of the Article IV consultations gave us a 2.5% GDP growth estimate for the year while an investment analyst earlier this week said we are on the brink of a recession.

These forecasts are difficult to substantiate but I believe the IMF team is in a better position than most of us to make a credible assessment of where we stand exactly. Still, I view the 2.5% growth figure as very pessimistic, hoping that it will pan out closer to 4%.

Of course, I do not have real statistics to base this on, but it is in line with the expenditure as announced in the budget. The immediate problem is not expenditure, this can be financed, rather it is sustainability in the face of a serious decline in government revenue.

The only dependable statistics we have to date are the adjusted macro-economic indicators as published in the final National Accounts for 2015/16. These, however, say nothing about this year. And even in this solid body of work, the adjustments tell a clear tale of down shifting. Whereas the annual GDP growth rate was first estimated at 6%, or close to it, the first adjustment brought this down to 5.7% and then finally to 5.3%. Now that is a serious adjustment. For anybody who understands indices, it translates to just over 14%, so do not be fooled by the 0,7% adjustment. That is a percentage point and not the real percentage decline.

So if our economy performed in real terms, almost 15% worse than expected, it means we have forfeited the real growth for the next three years. That is if your are lucky to maintain a 5% growth rate. And that is exactly what is happening to our economy. The actual investment rate has far exceeded the potential growth rate in the hope that the additional investment will have spurred a torrent of economic activity. It did not happen. The moment the state starting putting the brakes on liquidity, the engine stalled.

This is what happens where a government is directly involved for contributing 44% of GDP. Take your pick of any multiplier methodology and you will see that the secondary contribution is more than 60%. In short the government is directly or indirectly responsible for almost two thirds of economic activity and when such an overbearing entity hits a rough patch, the entire economy suffers.

Granted, we are not nearly in as bad a situation as Angola where the government is estimated to be more than 80% of the economy. This is also based on projections and estimates (there are no dependable statistics in Angola other than the size of the rulers’ offshore bank accounts) but if one considers the real effect their slump has on our northern trade, then it is patently obvious that they have an even more serious problem than us.

It is unfortunate that our economy is now in a classic boom bust cycle. But after six years of aggressive stimulation and additional liquidity, that is to be expected. For us, the capital market chickens have come home to roost this year.

The immediate drain of liquidity from the system has proven to be an enormous shock so far but I personally do not see such a gloomy picture. A very large part of the additional expenditure simply disappeared down the throats of the vast army of civil servant, but at least a not-insignificant amount went to fixed capital formation. This translates to a certain level of new or improved capacity which at some point will translate into additional economic activity, a rise in trade, a commensurate rise in government revenue, and, alas, a resumption of a liberal spending policy.

The only problem, as any analyst can point out, is that the timing of the anticipated return on investment is very difficult to predict. It may be towards the end of this year, it may be next year or it may only be in five years.

The good thing that has transpired this year is that a finance ministry can not pursue an aggressive stimulation policy without an adequately defined escape mechanism. We have run our noses into a wall and know we have lost our track.

In my view, the stimulation phase was needed. I fully supported the then finance minister in 2010 when she applied one of many new labels to come, – “counter-cyclical budgeting” and the magic of fiscal space. However, from the start it was obvious that there is no exit strategy. Budget after budget the expansionary phase got prolonged, every time under a new fancy label, until the latest for which everybody, both in government and in the private sector, is still wondering where all the money will come from.

One good thing to look forward to is that there will be no general elections for the next almost four years so there is no irrational need for pricey promises and reckless planning.