Diversification reduces investment risk Part 2

The passive investor who does not have the time and knowledge of financial markets should consider investing in multi-asset flexible portfolios typically offered by unit trust companies.

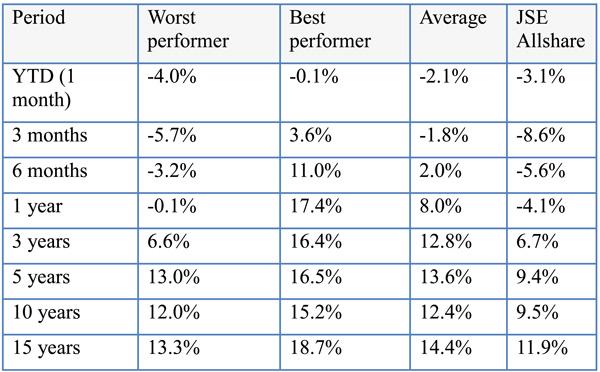

These are also typically employed by pension fund asset managers. The table below shows how successful these managers have been in achieving respectable returns for their pension fund members despite poor equity markets over various periods to end January 2016. While the equity market as a whole has not done well a number of times, asset managers have been able to move between equities, property, bonds and cash as well as between local and foreign investments and of course some have been very skillful in choosing shares that did well despite the market under-performing.

This comparative table shows the significant divergence between worst and best investment performers, the average returns, and the JSE Allshare Index performance.

Flexible diversification between different asset classes and different economies clearly reduces the risk of significantly underperforming the JSE and of delivering negative returns substantially. At the same time however, it reduces the opportunity of out-performance that should really only be the domain of an investment expert.

Conclusion

In the face of the head winds referred to above, investing in the right asset classes and in the right assets within each class is a skill that should still produce acceptable investment returns. By-and-large pension fund portfolio managers have not done a bad job, generally producing positive returns above inflation going by the average manager above. Of course some produced excellent results while others achieved dismal results as this table also shows. In the long run, pension funds are designed to achieve investment returns of about 5% to 6% above inflation to enable the pension fund member to retire in dignity. This is mostly the case for the average pension fund asset manager, and the exceptions per table above really only cover the very short term.

The investor should thus continue to focus on real returns and not be distracted by negative news and by short-term results. With an inflation rate now at around 5% with an investment return around 10% per annum. As an active fund member one should not shun equities but should be cautious and focus on stock picking. The commodity sector may offer selective buying opportunities but it may require patience to realise gains. The consumer facing increasing pains, and the fact that Consumer Goods and Consumer Services had a terrific run since the beginning of 2006, it is hard to see this sector continuing on its trajectory. The financial sector too is likely to suffer in sympathy with the consumer. The excessively depreciated Rand indicates that it should recover along with an increasing oil price and other commodities. The weak Rand eliminates the option of offshore diversification at this point in time. This leaves the Industrial sector as a sector we believe to also offer prospects, in the light of the weak Rand and low commodity prices.

In terms of diversification between different asset classes locally, the likelihood of further repo rate increases suggests that interest bearing investments do not hold good prospects at this stage. However the prospect of accelerating inflation favours inflation linked bonds.

Download the complete Benchtest fund investment overview at http://www.rfsol.com.na/benchmark

{kind=link}